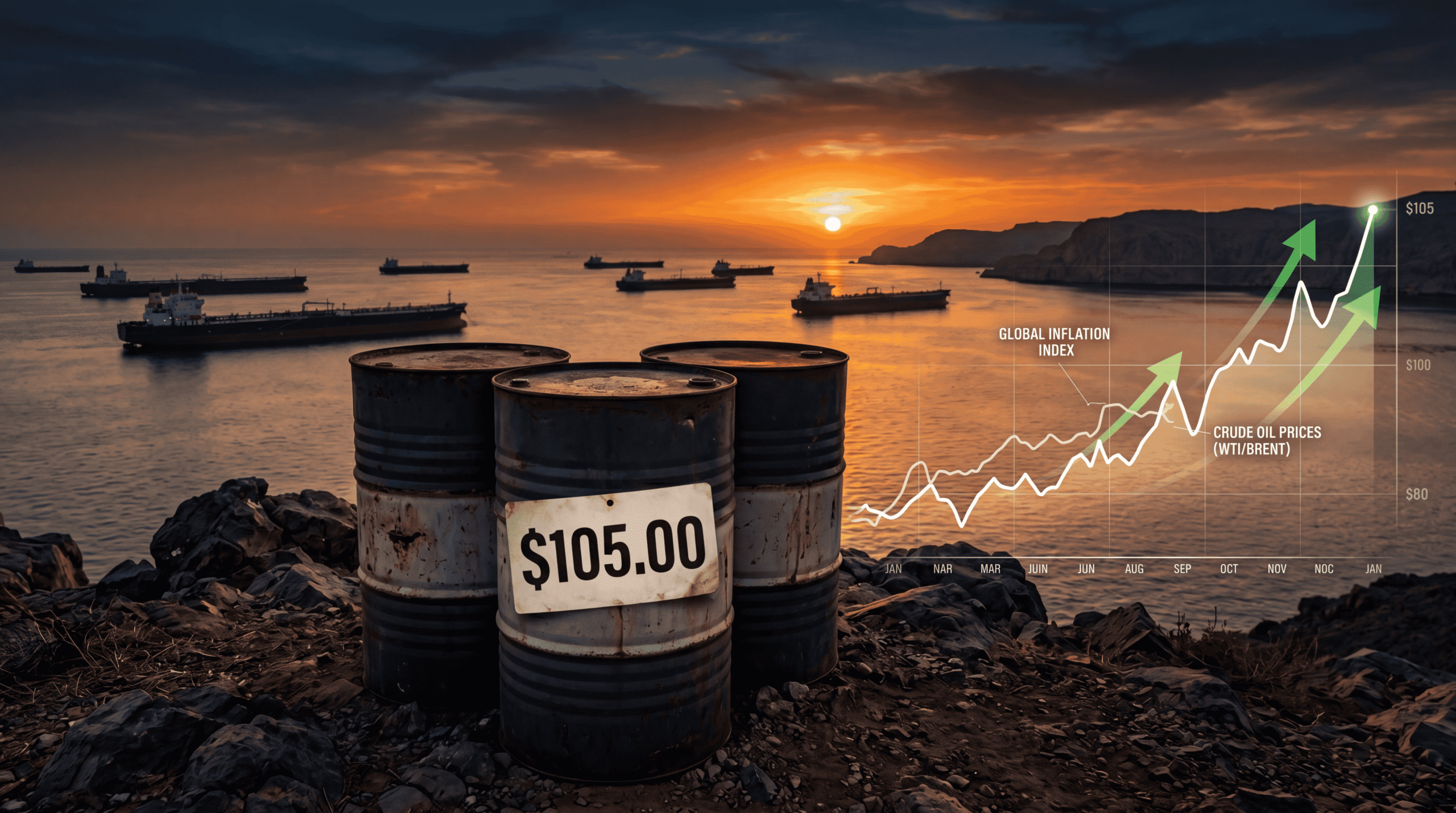

Here’s what Wall Street won’t tell you: the Iran war already broke something fundamental in the global economy, and no ceasefire will fix it quickly. After twenty years watching oil markets from Goldman Sachs trading floors to IMF crisis rooms, I can tell you this—when Brent crude jumps 44% in eight weeks to $105 per barrel, you’re not looking at a temporary shock. You’re looking at a structural break that will reshape American household budgets for the next eighteen months minimum.

The damage isn’t theoretical anymore. It’s in your gas tank at $4.06 per gallon. It’s in grocery aisles where diesel costs are quietly pushing up prices. And it’s about to get worse before it gets better, regardless of what happens in the Strait of Hormuz next week.

The Strait of Hormuz Chokepoint: Why 20% Matters More Than You Think

One-fifth of global oil flows through the Strait of Hormuz under normal conditions—that’s roughly 21 million barrels per day according to the U.S. Energy Information Administration. When that artery gets disrupted, even partially, the global economy doesn’t just slow down—it seizes up in ways that cascade through systems most people never see.

The World Bank’s latest Commodity Markets Outlook projects oil averaging $98-$102 per barrel through Q4 2026 if current disruptions persist. That’s not a spike—that’s a new plateau. Energy infrastructure across the Middle East has sustained damage that will take years to fully repair, not months.

Here’s the kicker: global oil production was running at 100 million barrels per day before the conflict. Current estimates from the International Energy Agency suggest we’re operating 3-4 million barrels below that capacity right now. That’s the equivalent of losing all of Canada’s oil exports overnight—and keeping them offline.

The Inflation Surge Nobody Saw Coming (Except We Did)

The Consumer Price Index hit 3.3% in March 2026—the highest reading since May 2024. But that’s yesterday’s news. The Personal Consumption Expenditures index, which the Federal Reserve actually uses to set policy, is projected to reach 4% by December according to the Cato Institute’s analysis. That’s double the Fed’s 2% target, and it puts Jerome Powell in an impossible position.

The Fed can’t cut rates to stimulate growth when inflation is running at 4%. They also can’t raise rates when GDP growth is already slowing to 1.8% for the year, down from 2.1% in 2025. This is the classic stagflation trap that haunted the 1970s—weak growth combined with persistent inflation. Post-Keynesian theory tells us this ends one of two ways: either through a deliberate recession that crushes demand, or through supply-side improvements that take years to materialize.

Energy inflation is particularly insidious because it’s regressive—it hits lower-income households hardest. Bureau of Labor Statistics data shows households in the bottom income quintile spend roughly 12% of their budget on energy and transportation, compared to 7% for top-quintile households. When gas goes from $2.98 to $4.06 per gallon, that’s not an inconvenience—it’s a financial crisis for millions of families.

What This Means For You: The Diesel Domino Effect

Forget gas prices for a moment. The real economic poison is diesel, which has climbed even faster than gasoline since the war started. Diesel powers the trucks that move 72% of America’s freight by weight, according to the Bureau of Transportation Statistics. When diesel costs surge, it creates a delayed inflation wave that hits grocery stores, Amazon deliveries, and retail shelves 4-8 weeks later.

Here’s your household impact translation: A family spending $300 weekly on groceries should expect that to rise to $320-$330 by mid-summer, even if food commodity prices stay flat. That $80-$120 monthly increase comes directly from transportation costs embedded in supply chains. Retailers will absorb some of the hit to maintain market share, but they’ll pass through 60-70% of diesel cost increases based on historical patterns.

Natural gas disruptions add another layer. The International Energy Agency’s April report warns that Middle East conflict will keep global natural gas supplies tight for two years. That matters because natural gas is the primary feedstock for fertilizer production. Fertilizer prices are already up 18% since February, and that flows directly into food costs with a 6-9 month lag.

The Fed’s Impossible Calculation

Jerome Powell is staring at a policy nightmare. Core PCE inflation—which strips out volatile food and energy—is cooling, dropping from 2.9% to 2.6% in recent months. That suggests underlying inflation pressures are moderating. But headline inflation, which includes the oil shock, is accelerating. Which one do you target?

The Fed’s dual mandate requires both price stability and maximum employment. Right now, the labor market is softening—initial jobless claims are trending up, and major tech firms are cutting thousands of jobs citing AI-driven efficiency gains. Bank of America’s internal spending data shows consumption growth is concentrated almost entirely in high-income households. Middle and lower-income Americans are already pulling back.

If the Fed holds rates steady at 4.5-4.75% (current range as of April 2026), they risk letting inflation expectations become unanchored. If they raise rates to combat energy-driven inflation, they could tip the economy into recession. Post-Keynesian analysis suggests the right move is to look through supply-side oil shocks and focus on core inflation—but that’s a politically radioactive position when voters see $4+ gas prices.

Why This Time Really Is Different

I’ve watched oil shocks for two decades—from the 2008 surge to $147/barrel to the 2014 crash to $26. This one has a different character. Previous spikes were driven by demand surges (2008) or OPEC production cuts (2014-2016). The Iran war represents actual physical destruction of production and refining capacity that can’t be quickly restored.

The IMF’s World Economic Outlook estimates that rebuilding Middle East energy infrastructure to pre-conflict capacity will require $80-120 billion in investment and 24-36 months of sustained effort. That assumes a stable security environment, which is far from guaranteed. Saudi Arabia’s Abqaiq facility, the world’s largest oil processing facility, can process 7 million barrels per day. If that or similar infrastructure sustains damage, you’re looking at multi-year disruptions.

Global spare oil production capacity—the ability to quickly ramp up output—is at its lowest level since 2008, hovering around 2.5 million barrels per day according to the IEA. That’s your cushion for handling disruptions, and it’s razor-thin. It means the market has no shock absorbers left. Any additional supply disruption, whether from hurricanes, industrial accidents, or geopolitical events, will spike prices immediately.

The Summer Travel Apocalypse

Jet fuel prices have jumped over $2 per gallon since late February, forcing airlines into aggressive cost recovery. United Airlines just raised checked bag fees by $10. Delta announced similar moves. American Airlines warned investors that fuel costs will be $800 million higher than planned for Q2 2026.

Those costs flow through to ticket prices with a 3-4 week lag. Memorial Day weekend bookings are already showing 22% higher average fares compared to 2025, according to travel data from Hopper. Summer vacation travel—a $140 billion annual industry in the U.S.—is about to become a luxury good for middle-class families who were already stretched thin.

The multiplier effects matter here. When families cut vacation spending, it hammers tourism-dependent economies from Florida to Hawaii to national park gateway towns. Those are service-sector jobs that can’t be offshored or automated. They disappear, and local economies contract.

What Happens Next: Three Scenarios

Scenario One: Rapid De-escalation (20% probability)

If a ceasefire materializes in the next 30 days and the Strait of Hormuz fully reopens, oil could decline to $85-90/barrel by Q3 2026. Gas prices would settle around $3.40-3.50/gallon by September. Inflation would moderate to 2.7-2.9% by year-end. GDP growth would still slow to 1.9-2.0%, but recession would be avoided. The Fed could cautiously cut rates by 25-50 basis points in late 2026. This is the optimistic case, and it requires geopolitical cooperation that looks increasingly unlikely.

Scenario Two: Frozen Conflict (55% probability)

More likely: fighting decreases but doesn’t end, Strait traffic remains partially disrupted, and oil trades in the $95-105 range through year-end. Gas stays above $3.80/gallon. PCE inflation hits 3.8-4.1% by December. GDP growth slows to 1.5-1.7%. The Fed holds rates steady, accepting above-target inflation to avoid triggering recession. Consumer spending weakens significantly in Q3-Q4 as real wages decline. Corporate profit margins compress. Stock market volatility increases. This is base case—uncomfortable but manageable.

Scenario Three: Escalation (25% probability)

If conflict spreads or critical infrastructure like Saudi Arabia’s Abqaiq facility is damaged, oil could spike to $130-150/barrel. Gas would exceed $5.50/gallon nationally, hitting $7+ in California and Northeast. PCE inflation would breach 5% by Q4. The economy would almost certainly enter recession in late 2026 or early 2027. The Fed would face the stagflation trilemma: high inflation, negative growth, and rising unemployment simultaneously. This scenario has no good policy responses—only choices about which pain to prioritize.

The Policy Failure Nobody Wants to Discuss

Here’s the uncomfortable truth: the U.S. Strategic Petroleum Reserve—designed exactly for this type of crisis—has been significantly depleted and hasn’t been adequately refilled. The SPR currently holds roughly 380 million barrels, down from 600+ million in 2020. At current consumption rates (about 20 million barrels per day), that’s 19 days of supply. It’s a cushion, not a solution.

The Biden administration sold SPR oil to moderate prices in 2022 during the Ukraine crisis. The Trump administration hasn’t replenished it meaningfully. Now, when you actually need the strategic reserve, it’s not there at full capacity. That’s a policy failure with bipartisan fingerprints, and it’s making this crisis worse than it needed to be.

What You Should Do Right Now

If you’re a CFO: Lock in fuel costs now if you haven’t already. Forward contracts at $105 oil look expensive today but will look smart in six months. Accelerate any planned price increases—your competitors are doing the same, and cost absorption will crater margins if you wait. Build inventory of any goods with high diesel transport costs. And stress-test your business model against $5.50/gallon gas and 4% inflation through Q1 2027.

If you’re an ordinary American: This isn’t the time for discretionary big purchases. Don’t buy that SUV. Don’t book that expensive summer vacation unless it’s already paid for. Build three months of expenses in savings if you haven’t already. If you’re in the market for a home, expect mortgage rates to stay elevated—the Fed isn’t cutting rates meaningfully while inflation runs hot. And if your job is in a cyclical industry (retail, hospitality, construction), make sure your resume is updated. The layoffs are just beginning.

The Bottom Line Wall Street Won’t Tell You

This oil shock is different because it’s a supply destruction event, not a demand fluctuation. Those take years to repair, not quarters. The inflation it’s creating is sticky—it embeds itself in wage expectations, rent increases, and price-setting behavior across the economy. Once inflation psychology shifts, it’s incredibly difficult to reverse without significant economic pain.

The era of $3 gas and 2% inflation is over for the foreseeable future. The new normal is higher energy costs, elevated inflation, and slower growth. That combination—what economists politely call “stagflation”—is the worst possible environment for financial markets and household finances. We saw this movie in the 1970s. It doesn’t end well without either a serious recession that crushes demand, or a supply-side miracle that dramatically increases energy production.

Neither looks likely in the next twelve months. The Iran war may have lasted only eight weeks so far, but its economic aftermath will define 2026 and stretch well into 2027. The damage isn’t temporary, the recovery won’t be quick, and the people telling you otherwise are either uninformed or selling you something.

The smart money is already positioned for a long, uncomfortable adjustment period—and you should be too.