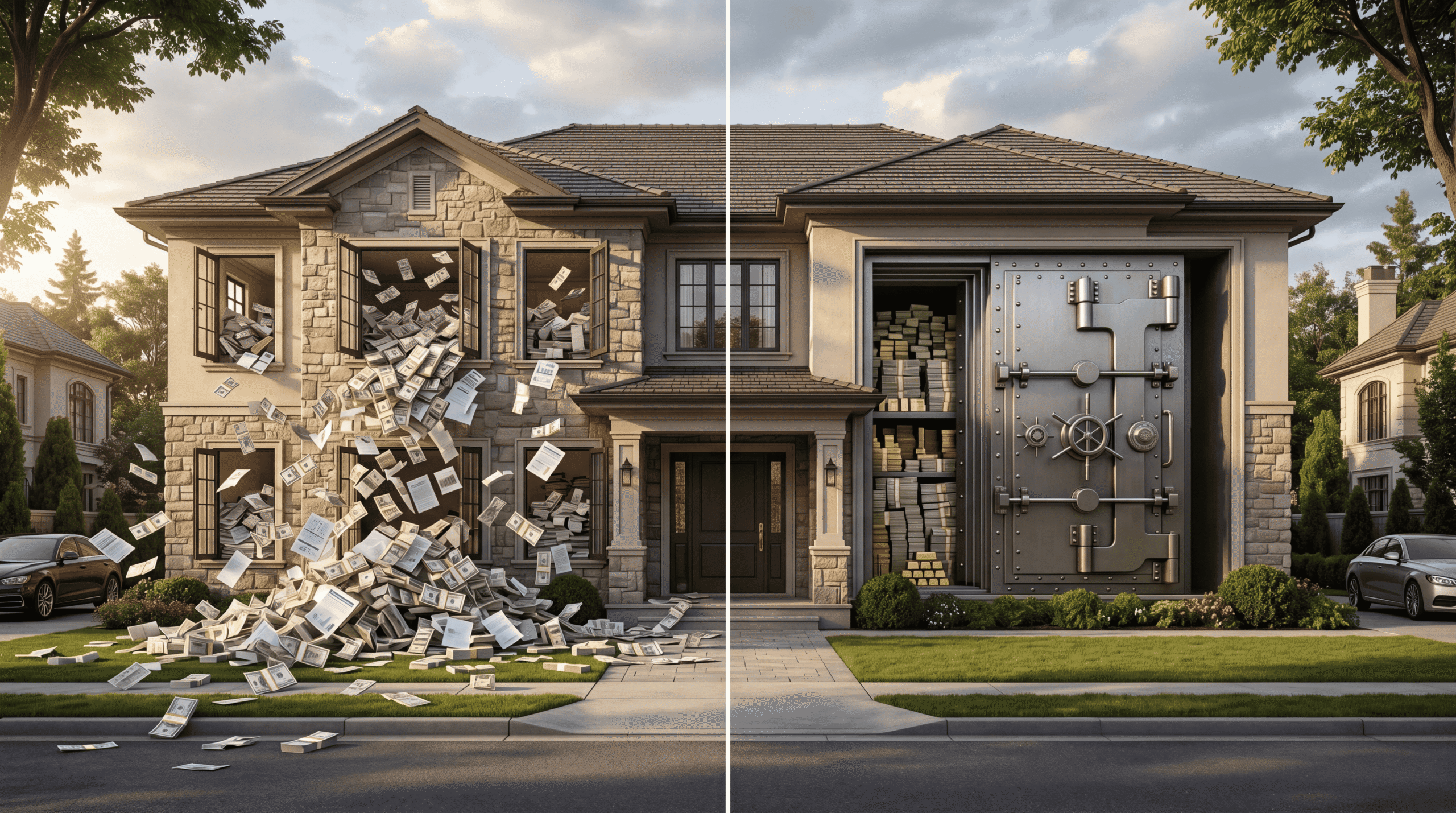

Your retirement account looks impressive on paper. Your home equity has doubled. Your net worth spreadsheet says you’re crushing it. So why does your checking account make you anxious every month?

Because you’ve fallen for the greatest financial illusion in America: confusing assets you can’t touch with wealth you can actually use. Wall Street calls this being “asset rich, cash poor.” I call it exactly what it is—broke with a good credit score.

The Trap Every Middle-Class American Falls Into

Here’s the uncomfortable truth: Federal Reserve data shows that while the median American household net worth hit $192,900 in 2022, nearly 40% of Americans couldn’t cover a $400 emergency without borrowing money. How is that mathematically possible?

Simple. Most of that “wealth” is locked in places you can’t access without penalties, taxes, or selling your primary residence. Your 401(k) might say $250,000, but try withdrawing $20,000 before age 59½. After the 10% penalty and your marginal tax rate, that’s actually $13,500. Your home equity is even worse—it costs you money every single month in property taxes, insurance, and maintenance while producing zero cash flow.

The wealthy don’t make this mistake. They understand a fundamental principle that financial advisors won’t tell you: liquidity is wealth, not net worth.

The Psychology Trap: Why We Optimize for the Wrong Number

I’ve watched countless families optimize for a number on a retirement statement while living paycheck to paycheck. Why? Because every financial institution has incentivized you to focus on the wrong metric.

Your bank wants you to see that mortgage balance shrinking—it makes you feel accomplished while they collect interest for 30 years. Your brokerage celebrates when your portfolio hits new highs—while charging fees on assets you can’t use. Your financial advisor congratulates you on “maxing out” your 401(k)—while you’re eating ramen and turning down opportunities because you have no accessible capital.

This is behavioral economics at work. Researchers call it “mental accounting”—we treat money differently based on where it’s stored rather than its actual utility. Studies in behavioral finance show that people feel wealthier when they see large account balances, even if accessing that money would destroy 30-40% of its value.

Meanwhile, the actual wealthy focus on a completely different metric: how much capital can I deploy this month without penalties or selling assets at a loss?

What Americans Get Wrong About Building Wealth

The standard American wealth-building playbook is fundamentally broken. You’re told to:

1. Max out your 401(k) first (locking away capital for 30+ years)

2. Pay down your mortgage aggressively (converting cash into illiquid home equity)

3. Keep 3-6 months emergency fund (the only liquid asset you’re allowed)

4. Invest everything else in index funds (inside tax-advantaged accounts you can’t touch)

This advice creates exactly what we’re seeing: Americans with impressive net worth statements and empty checking accounts. Your money is working for future you while present you is stressed about a car repair.

The math seems sound until you realize what you’re sacrificing. When you lock away $20,000 annually in a 401(k) from age 30 to 65, yes, it might grow to $2.1 million at 7% returns. Congratulations—you’ll be rich when you’re 65.

But what about the business opportunity at age 35 that required $50,000? The real estate deal at 42? The career transition at 48 that needed 12 months of runway? You couldn’t access your capital without devastating penalties, so you stayed stuck. That immobility has a cost that never appears in retirement calculators.

The Real Cost of Illiquid Wealth

Being paper wealthy but cash poor doesn’t just create stress—it actively makes you poorer. Here’s how:

You pay the “broke tax” constantly. Can’t cover an unexpected expense? You’re paying 24% APR on a credit card. Need to replace your car? You’re financing at 7% instead of paying cash. Your water heater dies? You’re on a payment plan at the plumber’s markup price.

According to Pew Research, the average American household with credit card debt pays over $1,000 annually in interest. That’s $1,000 of wealth destruction that happens because you have $200,000 in a 401(k) but $3,000 in your checking account.

You miss wealth-building opportunities. Real wealth isn’t built by slowly accumulating in index funds. It’s built by having capital available when asymmetric opportunities appear. Every wealthy family I’ve worked with has a story about deploying cash during the 2008 crash, or funding a business, or buying real estate below market value. You can’t do any of that when your wealth is locked away.

You make fear-based decisions. When you’re cash-poor despite being “wealthy” on paper, you operate from scarcity. You stay in jobs you hate because you can’t afford a transition period. You don’t negotiate aggressively because you’re scared of losing income. You avoid calculated risks because your emergency fund is already stressed. This mindset costs you millions in lifetime earnings.

What To Do Instead: The Liquidity-First Approach

Wealthy families structure their finances completely differently. They optimize for liquidity and optionality first, then tax-advantaged growth second. Here’s the framework:

Step 1: Build a 12-month opportunity fund, not a 3-month emergency fund. Before you put another dollar in your 401(k) beyond the employer match, accumulate 12 months of expenses in a high-yield savings account. Yes, 12 months. This isn’t pessimism—it’s buying yourself freedom. Current rates are above 4% APY. That’s not exciting, but it’s liquid, safe, and available instantly.

This fund isn’t just for emergencies—it’s for opportunities. It lets you negotiate from strength. It lets you make career moves. It lets you deploy capital when everyone else is panicking.

Step 2: Stop aggressively paying down low-interest debt. If your mortgage is at 3%, paying it off early is a terrible use of capital. You’re converting liquid cash into illiquid home equity while earning a 3% “return.” That same capital could be generating income, funding investments, or sitting ready for opportunities. Make your minimum payment and redirect that extra cash to liquid assets.

Step 3: Rebalance your 401(k) contributions. Yes, I’m saying reduce them if you’re cash-poor. Take enough to get the full employer match—that’s still a 50-100% instant return. But every dollar beyond that should go toward building liquidity until you have that 12-month fund. The tax deduction isn’t worth being broke.

Here’s the math everyone ignores: Putting $10,000 in a 401(k) saves you maybe $2,400 in taxes (at 24% marginal rate). But if that $10,000 in liquid savings prevents you from putting $5,000 on a credit card at 24% APR, you’re actually ahead. And that’s before counting the opportunity cost of not having capital available.

Step 4: Build income-producing liquid assets. Once you have your opportunity fund, focus on assets that generate cash flow and remain liquid. That might be a taxable brokerage account with dividend-paying stocks. It might be I-bonds (currently yielding inflation-adjusted returns). It might be investing in short-term real estate debt or being a silent partner in small businesses.

The key: these assets should be accessible within 30-90 days maximum, and they should be producing income now, not just decades from now.

The Controversial Truth About Retirement Accounts

The 401(k) system was never designed to be the primary wealth-building vehicle for Americans. It was created in 1978 as a supplementary tax dodge for executives. Somehow it became the entire retirement strategy for the middle class—which is incredibly convenient for employers who no longer have to fund pensions.

Here’s what your financial advisor won’t tell you: Wealthy families don’t have the majority of their wealth in retirement accounts. According to Federal Reserve data, households in the top 10% by wealth have only 22% of their assets in retirement accounts. The middle class? Over 60%.

Why? Because the wealthy understand that control and access matter more than tax deductions. They’d rather pay tax now and have complete liquidity than save 24% on taxes but lock away capital until age 60.

I’m not saying never use retirement accounts. I’m saying they should be part of a liquidity-first strategy, not the foundation of it. Get your match. Then max out Roth IRAs (at least you can withdraw contributions without penalty). But don’t sacrifice liquidity just to lower this year’s tax bill.

The Real Definition of Financial Security

Financial security isn’t a net worth number. It’s answering “yes” to these questions:

• Can you cover 12 months of expenses without touching investments?

• Can you deploy $20,000-50,000 on an opportunity within a week?

• Can you survive losing your job without panic?

• Can you make career or business moves without being forced by cash flow?

• Do unexpected expenses create inconvenience rather than crisis?

If you have $300,000 in retirement accounts but answered “no” to these questions, you’re not wealthy—you’re just house-poor with extra steps.

The families I work with who sleep soundly at night aren’t the ones with the highest net worth. They’re the ones with the most liquidity relative to their lifestyle. They have cash. They have investments they can sell without penalty. They have credit lines they never use. They have optionality.

That’s real wealth.

What This Looks Like in Practice

Let me give you two scenarios with the same income:

Scenario A (Traditional Advice):

Sarah makes $120,000. She maxes out her 401(k) at $23,000 annually, pays an extra $1,000/month on her mortgage principal, and keeps $15,000 in savings. Her net worth is growing beautifully. On paper, she’s doing everything right.

Then her company announces layoffs. She has 3 months of expenses in savings and starts panicking immediately. She can’t access her 401(k) without penalties. Her home equity can’t pay bills. She takes the first job offer she gets—at $95,000, a $25,000 pay cut—because she’s terrified. Over the next decade, this decision costs her $250,000+ in lifetime earnings.

Scenario B (Liquidity-First):

Mike makes $120,000. He contributes enough to his 401(k) to get the full match ($9,000), makes minimum payments on his 3.5% mortgage, and builds a liquid savings and investment account to $80,000 over 3 years. His net worth grows more slowly than Sarah’s on paper.

When his company announces layoffs, he’s calm. He has 18 months of runway. He takes time to find the right role, negotiates aggressively, and lands a position at $140,000. He also has the capital to start a side business that generates an additional $30,000 annually. Over the next decade, this optionality creates $500,000+ in additional wealth.

Who was actually wealthier? The math is unambiguous.

Your Next Move

This week, calculate your liquidity ratio: liquid assets (checking, savings, taxable investments you could sell immediately) divided by monthly expenses. If that number is under 12, you have work to do.

Here’s your action plan:

1. Reduce 401(k) contributions to employer match level only

2. Stop extra mortgage payments completely

3. Redirect that cash flow to a high-yield savings account

4. Build toward 12 months of expenses in liquid assets

5. Only after hitting that milestone increase retirement contributions

Yes, this will feel wrong. You’ve been told your whole life that maxing out retirement accounts is the responsible thing to do. But responsible financial planning isn’t about optimizing for the biggest number on a statement you can’t access. It’s about building real security and real optionality.

The wealthy have always known this. Now you do too.