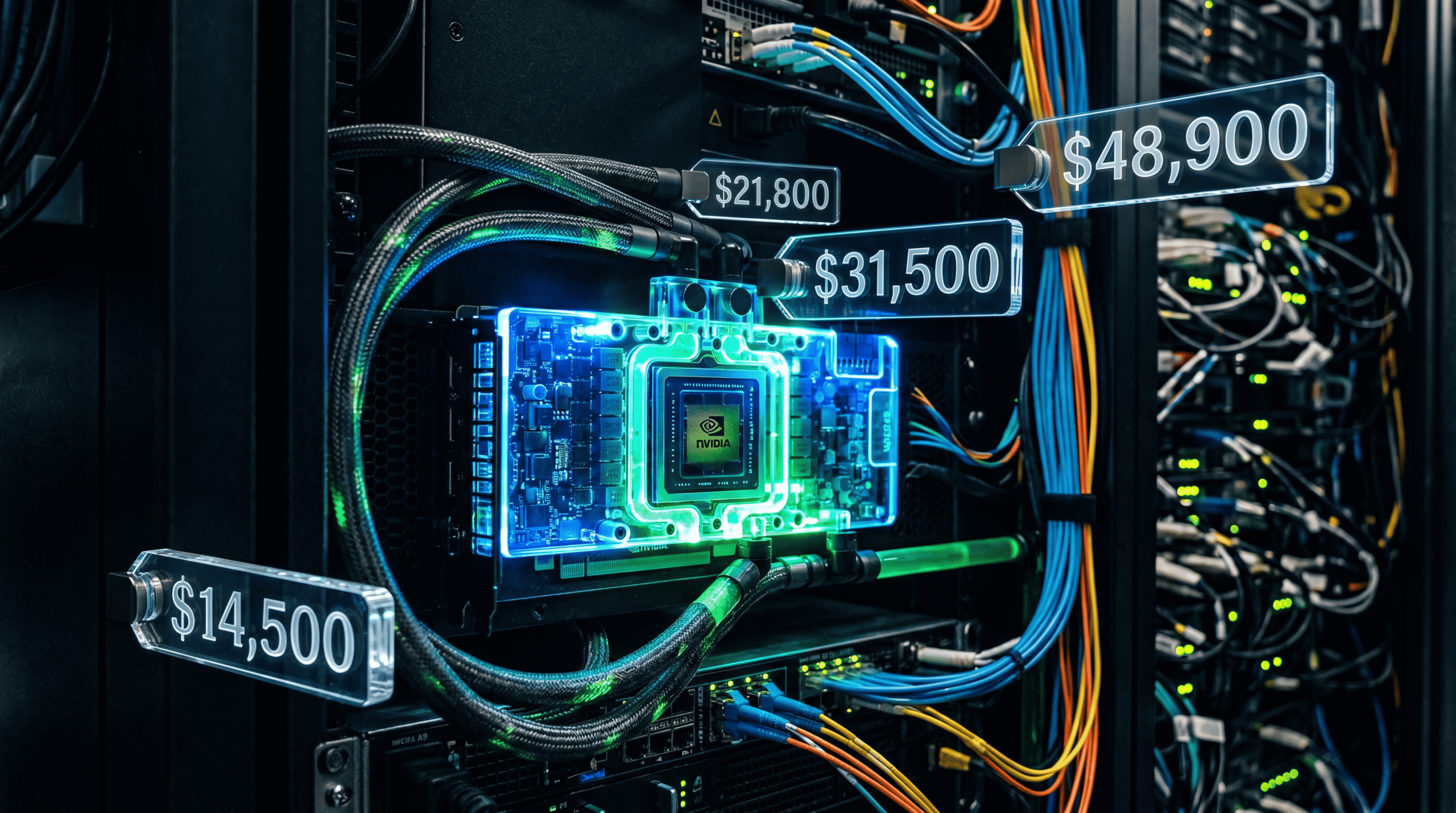

Every tech exec I talk to is panicking about AI chip prices. NVIDIA’s H100 street prices hit $40K in late 2024, up from $25K at launch. But here’s what nobody wants to admit: this isn’t a supply problem. It’s an allocation problem, and the companies stockpiling chips right now are making the same mistake enterprises made hoarding servers in 2007, right before AWS proved you didn’t need to own the metal.

The press keeps calling this a shortage. It’s not. It’s a rebalancing of who gets to build AI infrastructure, and if you’re a mid-market company writing checks for H100s right now, you’re probably on the wrong side of that shift.

What The Press Got Wrong About AI Chip Economics

When Bloomberg reports “AI chip shortage drives prices up 60%,” they’re missing the actual story. Yes, H100 prices jumped from $25K to $40K in twelve months. But demand isn’t the constraint—allocation is.

Here’s what’s actually happening: NVIDIA isn’t rationing chips because TSMC can’t make enough. They’re rationing because hyperscalers (Amazon, Microsoft, Google, Meta) locked in massive multi-year purchase agreements that give them first access to every new fabrication run. The remaining supply gets distributed through a Byzantine system of regional distributors, systems integrators, and resellers—each taking their cut.

I watched this play out at my last startup. We got quoted $32K per H100 through an authorized reseller in Q3 2024. By the time we were ready to buy in Q4, same reseller wanted $43K. Not because NVIDIA raised prices—their list price stayed at $25K-$30K for volume orders. The markup came from middlemen realizing they could extract more from desperate AI labs.

The Real Technical Constraint Nobody Talks About

But here’s the part that matters if you’re actually building something: chip prices are a distraction from the real bottleneck, which is integration complexity.

Getting an H100 into production isn’t like adding RAM to a server. You need:

- InfiniBand or 400GbE networking infrastructure (add $15K-$50K per node)

- Liquid cooling systems for any serious cluster (most datacenters don’t have this)

- Power delivery that can handle 700W sustained per GPU

- Software stack that can actually utilize NVLink and Tensor Cores efficiently

I talked to an ML infrastructure lead at a Series B company last month. They spent $800K on 20 H100s. Six months later, their actual utilization is 31% because their training pipeline wasn’t designed for tensor core operations and their data loading is still the bottleneck. They would have been better off spending $200K on A100s and $600K on hiring someone who knows how to optimize CUDA kernels.

Why AMD and Alternative Chips Aren’t The Answer You Think

Every founder asks me: “Should we just buy AMD MI300X instead?” The MI300X specs look competitive—192GB of HBM3 memory versus H100’s 80GB, similar compute throughput for many workloads. And street prices are 20-30% lower.

Here’s why that doesn’t matter for most companies: software ecosystem lock-in is the real moat. NVIDIA’s CUDA platform has 15 years of optimization libraries, kernel implementations, and tribal knowledge. AMD’s ROCm is improving fast, but switching means rewriting parts of your training pipeline and debugging obscure compatibility issues.

The calculus changes if you’re training foundation models where you control the entire stack. But if you’re fine-tuning Llama or building on top of existing frameworks, CUDA’s ecosystem advantage is worth the premium for most teams.

Google’s TPUs tell a different story. TPU v5p pods are genuinely competitive for transformer workloads, and you don’t pay for the chips—you rent compute time. But you’re locked into Google Cloud’s infrastructure and their software stack. For many companies, that’s a bigger risk than NVIDIA’s pricing.

What Chip Integration Actually Means For Your Product Timeline

Let’s talk about what nobody mentions in these breathless AI chip articles: time to production.

If you order H100s today through standard channels, you’re looking at:

- 4-6 weeks for delivery (if you’re lucky)

- 2-4 weeks for datacenter integration and testing

- 2-8 weeks debugging networking, drivers, and thermal issues

- Then you can start actually training models

That’s 2-4 months of calendar time before you run your first real workload. During which your team is burning runway and your H100s are depreciating assets sitting in a rack.

Compare that to spinning up an AWS P5 instance with H100s: you’re running code in 10 minutes. Yes, you pay $98/hour instead of $40K upfront. But you also skip three months of integration hell, and you can scale up or down based on actual usage patterns instead of guessing how many chips you need.

I’ve seen exactly one case where buying made sense: a Series C company training proprietary models 24/7 for 18+ months. Their math showed breakeven at 11 months versus cloud rental. Everyone else I’ve advised? Cloud makes more sense, even at current pricing.

Who Actually Wins and Loses From This Price Surge

Winners:

- Hyperscalers (Amazon, Microsoft, Google): They locked in allocation agreements 18-24 months ago at lower prices. Now they’re re-selling that compute at 2-3x markup through cloud services while their competitors scramble for chips.

- NVIDIA’s partners in China: Loopholes in export controls mean modified H100 variants flow to Chinese AI labs at massive premiums. Some chips are selling for $60K+ in mainland China.

- Systems integrators: Companies like Lambda Labs, CoreWeave, and Crusoe Energy that bought early and can offer immediate access are printing money right now.

Losers:

- Mid-market AI companies: Too small for direct NVIDIA relationships, too large to make cloud economics work cleanly. They’re stuck paying street prices to resellers while competing with hyperscalers who have better chip access.

- Traditional hardware manufacturers: Dell, HPE, and Supermicro are scrambling for allocation just like everyone else. Their manufacturing scale doesn’t matter when NVIDIA controls the tap.

- Companies that bought too early: If you stockpiled A100s in 2023 thinking you’d have an advantage, you’re now stuck with last-generation chips while everyone else is standardizing on H100s. Your resale value is dropping fast.

The Allocation Game You Should Actually Be Playing

Here’s what sophisticated teams are doing instead of panic-buying chips:

1. Optimize for the hardware you can actually access. If you can get consistent access to AWS P5 instances, design your training pipeline around that instead of waiting for H100s to ship. I know teams that rewrote their data pipeline to use streaming instead of batch loading and cut their training time by 40%—no new hardware required.

2. Use cloud for spiky workloads, buy for baseline load. If you need 4 H100s running 24/7 and occasionally burst to 32 for experiments, buy 4 and rent the rest. This is the opposite of what most companies do (they buy peak capacity and let it sit idle).

3. Lock in multi-year cloud commitments now. AWS and Azure are offering significant discounts for 3-year reserved instance commitments on AI accelerator instances. If you know you’ll need compute long-term, these agreements give you price protection against future increases.

4. Invest in software optimization before hardware. Most ML teams are getting 30-50% utilization from their GPUs because of inefficient data pipelines, poor kernel implementations, or suboptimal batch sizes. Hiring one senior CUDA engineer will likely give you more performance than buying two more H100s.

What Customers Should Actually Expect In 2025

The narrative that chip prices will normalize once “supply catches up” is wrong. This isn’t a temporary shortage—it’s a permanent rebalancing of who gets to build AI infrastructure.

Expect:

- Street prices stay elevated through 2025: Even as NVIDIA ramps H200 and B100 production, hyperscaler commitments will absorb most supply. The delta between list and street price won’t close.

- More creative financing: Chip-as-a-service, revenue sharing agreements, and lease-to-own options will proliferate. This is good—it means you don’t need $2M in capital to get started.

- Consolidation of compute providers: Small GPU clouds will get acquired or go under. The survivors will be hyperscalers, specialized AI clouds with strong unit economics (like CoreWeave), and a few niche players with unique offerings.

- Software becomes the real differentiator: As everyone gets access to similar hardware (either through purchase or cloud), the competitive advantage shifts entirely to who can extract the most performance from each chip.

The Uncomfortable Truth About AI Infrastructure

Here’s what I tell founders who ask about chip strategy: if your competitive advantage depends on owning hardware, you don’t have a competitive advantage.

The companies winning in AI aren’t the ones with the most GPUs. They’re the ones with the best algorithms, the cleanest data pipelines, and the deepest understanding of their domain. OpenAI doesn’t win because they have more compute than Google (they don’t). They win because they figured out how to align language models better than anyone else.

Yes, you need compute. But you need it to iterate fast and learn, not to build a moat. Every dollar you spend on chips sitting in your datacenter is a dollar you’re not spending on the engineers and researchers who actually create value.

The chip price surge is real. But it’s also a distraction from what actually matters: can you build something people want, and can you do it before you run out of money? If you’re solving the chip problem before the product-market-fit problem, you’ve already lost.

The contrarian take for 2025: The companies that win the AI race won’t be the ones that bought the most chips in 2024—they’ll be the ones that didn’t buy any, because they were too busy shipping products on rented cloud instances while their competitors were stuck in procurement hell.