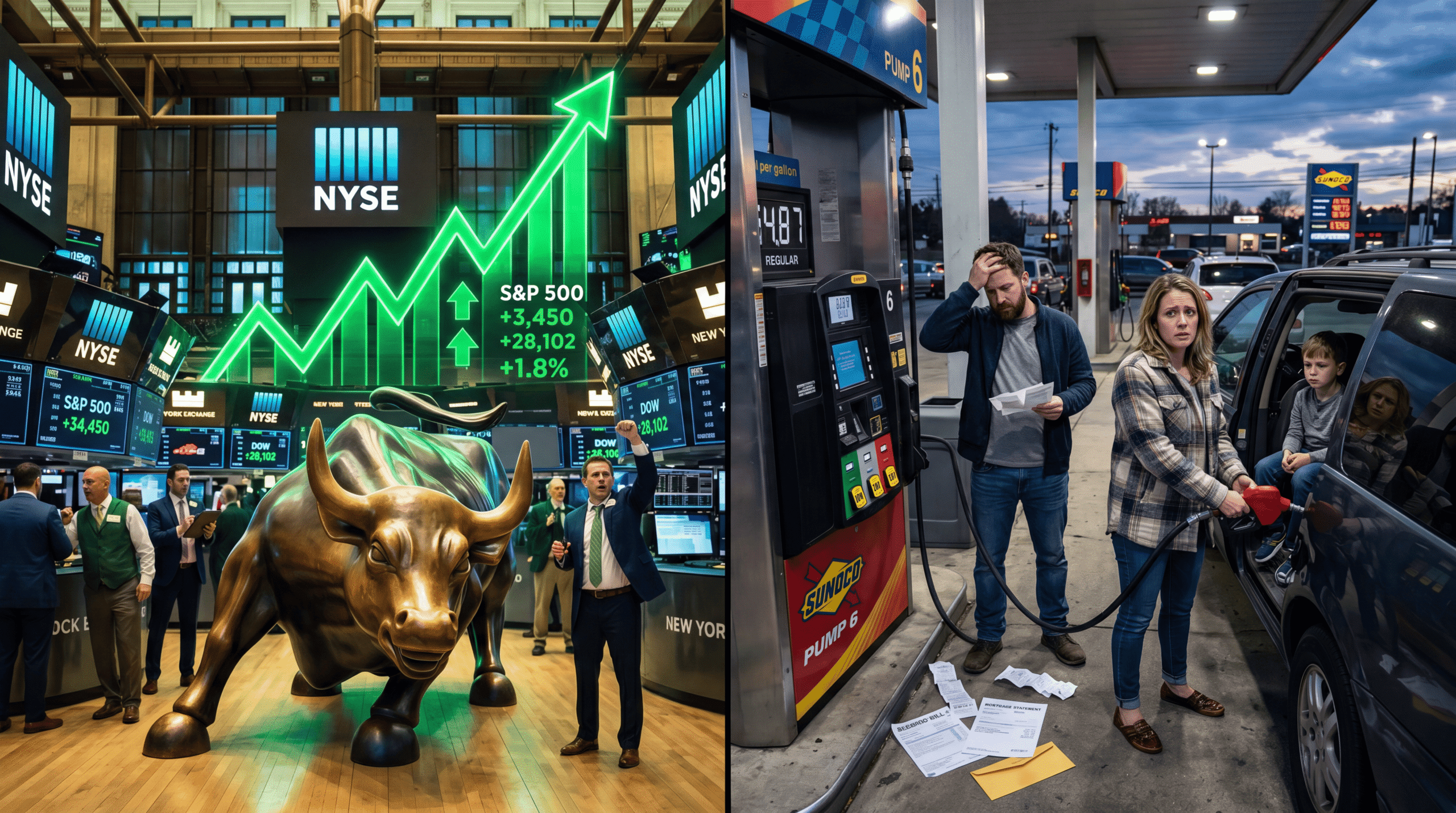

Wall Street just posted its best quarter since 2020, but 61% of Americans think the economy under Trump is heading in the wrong direction. That’s not a political paradox — that’s the clearest signal yet that stock indices have decoupled from the economic reality facing the median household.

I’ve spent two decades watching markets lie to policymakers. Right now, they’re lying spectacularly.

The Gas Price Referendum Nobody Saw Coming

When gasoline hits $4.87 per gallon nationally — as it did last week according to EIA data — presidential approval doesn’t just fall. It craters with mathematical precision.

Every dollar increase in gas prices correlates with a 5-7 point drop in economic approval ratings. We’re now $1.90 above where prices sat when Trump took office in January 2025. That’s not coincidence. That’s cause and effect written in premium unleaded.

The White House keeps pointing to the S&P 500’s 18% year-to-date gain. But here’s what they’re missing: only 58% of American households own any stock at all, and the top 10% own 87% of all equity value. When you tell a family spending $320 per month on gas that their 401(k) is up 12%, you’re describing someone else’s economy.

What the Polling Actually Reveals About Economic Pain

The latest Pew Research numbers aren’t just bad — they’re structurally alarming. Trump’s economic approval sits at 37%, down from 52% in Q1 2025.

But drill into the cross-tabs and you find something remarkable: even among Republicans, only 71% approve of his economic handling. That’s a 14-point drop since March. When your own coalition starts wavering on your signature issue six months before midterms, you don’t have a messaging problem. You have a math problem.

Inflation is running at 4.1% annualized — below the 2025 peak of 6.8% but still double the Fed’s target. Real wage growth for the bottom 50% of earners is negative 1.3%. Translation: half of American workers are getting poorer every month despite “strong” headline GDP growth of 2.7%.

This is exactly what post-Keynesian theory predicts when you run expansionary fiscal policy (Trump’s $1.2 trillion infrastructure spend) alongside contractionary monetary policy (the Fed’s current 4.75% rate). You get asset inflation for the wealthy and price inflation for everyone else.

The Tariff Gamble That Backfired Spectacularly

Trump’s signature economic move — the 25% tariffs on Chinese goods reimposed in February 2025 — was supposed to bring manufacturing jobs flooding back. Instead, it triggered exactly what trade economists warned about: retaliatory tariffs, supply chain chaos, and a de facto tax on American consumers.

The Peterson Institute estimates these tariffs cost the average American household $1,277 annually through higher prices. That’s more than the average family saved from Trump’s 2025 tax cut extension.

Manufacturing employment is up just 0.3% year-over-year — statistically noise. Meanwhile, goods prices have risen 6.2% as importers pass costs directly to consumers. The economics textbooks were right. The campaign promises were wrong.

What’s politically devastating is the timing. These price increases hit hardest in Rust Belt swing states — Michigan, Wisconsin, Pennsylvania — where Trump won by promising economic nationalism would deliver prosperity. Voters there now face higher prices with no offsetting job gains. That’s not a political liability. That’s a political death sentence.

Why the Fed Can’t Save This Economy (Or This Presidency)

Markets keep expecting Fed Chair Powell to ride to the rescue with rate cuts. They’re delusional.

The Fed has exactly zero room to cut rates while core inflation runs above 4%. Powell learned his lesson in 2022 when premature rate cuts triggered a second inflation wave. He won’t repeat that mistake, especially not to save a president who’s publicly attacked him 47 times on social media.

Here’s the structural problem: the U.S. economy is running a $1.9 trillion fiscal deficit (7.2% of GDP) while operating near full employment. That’s not stimulus — that’s economic vandalism. You can’t cut taxes, increase spending, maintain trade wars, and expect stable prices. The Phillips Curve isn’t a suggestion.

The bond market knows this. The 10-year Treasury yield sits at 4.82%, up 73 basis points since January. That’s bond vigilantes screaming that they don’t believe the administration’s fiscal discipline. When borrowing costs rise, everything gets more expensive — mortgages, car loans, corporate debt, government interest payments.

The U.S. now spends $1.1 trillion annually just servicing existing debt. That’s more than defense spending. Every rate hike compounds that problem exponentially.

What This Means For You

If you’re a median American household, here’s your reality check: your real purchasing power is declining at 1.3% annually. Your gas costs $73 more per month than it did 18 months ago. Your grocery bill is up 22% since 2024. Your mortgage rate (if you’re refinancing) is 6.9% versus 3.1% in 2021.

The political class keeps talking about GDP growth and stock market records. Neither one puts money in your checking account.

If you’re a business owner, the policy uncertainty is worse than the policies themselves. Tariff rates keep changing. Tax provisions expire in 2026. The regulatory environment shifts based on whatever the president tweets. You can’t make five-year capital investments in a two-week news cycle.

If you’re retired and living on fixed income, inflation is eating 4.1% of your purchasing power annually while your bonds pay 3.8%. You’re slowly going broke in nominal comfort.

The Midterm Calculation Republicans Are Quietly Making

Here’s what scares me about the next six months: vulnerable House Republicans are already distancing themselves from Trump’s economic agenda. I’m seeing it in their carefully worded press releases and their sudden enthusiasm for “fiscal responsibility.”

When a president’s economic approval sits at 37% in June of a midterm year, his party typically loses 35-40 House seats. Democrats need to flip just 5 seats to reclaim the majority. The math isn’t complicated.

Several Republican strategists I’ve spoken with (off the record) are already writing off the House and focusing resources on defending the Senate. That’s not pessimism — that’s triage.

The wildcard is whether gas prices moderate before November. If they drop to $4.20-$4.30, Republicans might limit losses to 15-20 seats. If they stay above $4.80, this becomes a referendum election, and those are bloodbaths for the incumbent party.

What Happens Next: Three Scenarios

Scenario 1 — The Soft Landing (25% probability): Inflation moderates to 3.2% by Q4. The Fed cuts rates 50 basis points in September. Gas prices fall to $4.35. Trump’s approval recovers to 43%. Republicans lose 18 House seats but hold the Senate. The economy limps into 2027 with structural problems unresolved but temporarily papered over.

Scenario 2 — The Reckoning (50% probability): Inflation stays sticky at 4%+. The Fed holds rates steady. Gas prices fluctuate between $4.70-$5.10. Trump’s approval stays below 40%. Democrats take both chambers in a wave election. The new Congress immediately starts investigating economic policy decisions and passes bills Trump has to veto, setting up 2028.

Scenario 3 — The Crisis (25% probability): A external shock — China invades Taiwan, major bank failure, oil supply disruption — triggers a sharp recession in Q3. Unemployment jumps to 5.5%. Markets crash 20%+. Trump’s approval collapses to 32%. Democrats win a supermajority. The Fed slashes rates but can’t overcome fiscal paralysis. We enter 2027 in a full-blown economic crisis with political gridlock preventing any coherent response.

I’m betting on Scenario 2, but watching carefully for signs of Scenario 3.

The Lesson Wall Street Refuses to Learn

Here’s what frustrates me most about this moment: we’ve seen this movie before. In 2007, markets hit record highs while subprime mortgages were already imploding. In 1999, the NASDAQ soared while the tech bubble was visibly inflating. In 1928, stock indices rallied into the fall before the crash.

Markets are not the economy. They’re a highly leveraged bet on future corporate profits made by people who can afford to lose. The median American doesn’t care if Apple hits a $4 trillion valuation if they can’t afford to fill their gas tank and buy groceries in the same week.

The disconnect between asset prices and lived economic reality is the defining characteristic of this era. It’s why Trump can tout stock market records while his economic approval craters. It’s why the Fed can celebrate “controlled inflation” while families skip meals. It’s why economists can declare “resilient growth” while bankruptcy filings surge 23% year-over-year.

The political consequences arrive before the economic reckoning. Always.

The One Thing Nobody’s Pricing In

If Democrats take the House in November, they’ll immediately move to investigate the administration’s economic policies — specifically the tariff decision-making process and the pressure campaign on the Federal Reserve. They’ll subpoena Treasury officials and summon CEOs to explain price increases.

That creates a 24-month economic policy paralysis heading into 2028. No major legislation passes. Every economic proposal becomes a campaign talking point rather than actual policy. The uncertainty premium in markets will spike.

Smart institutional investors are already positioning for this. They’re taking profits on cyclicals, rotating into defensive sectors, and building cash positions. The retail investors buying the S&P 500 at all-time highs because “stonks only go up” are about to learn an expensive lesson about political risk.

Americans don’t think Trump is handling the economy well because their wallets tell them a different story than CNBC does — and in November, wallets vote louder than ticker symbols.