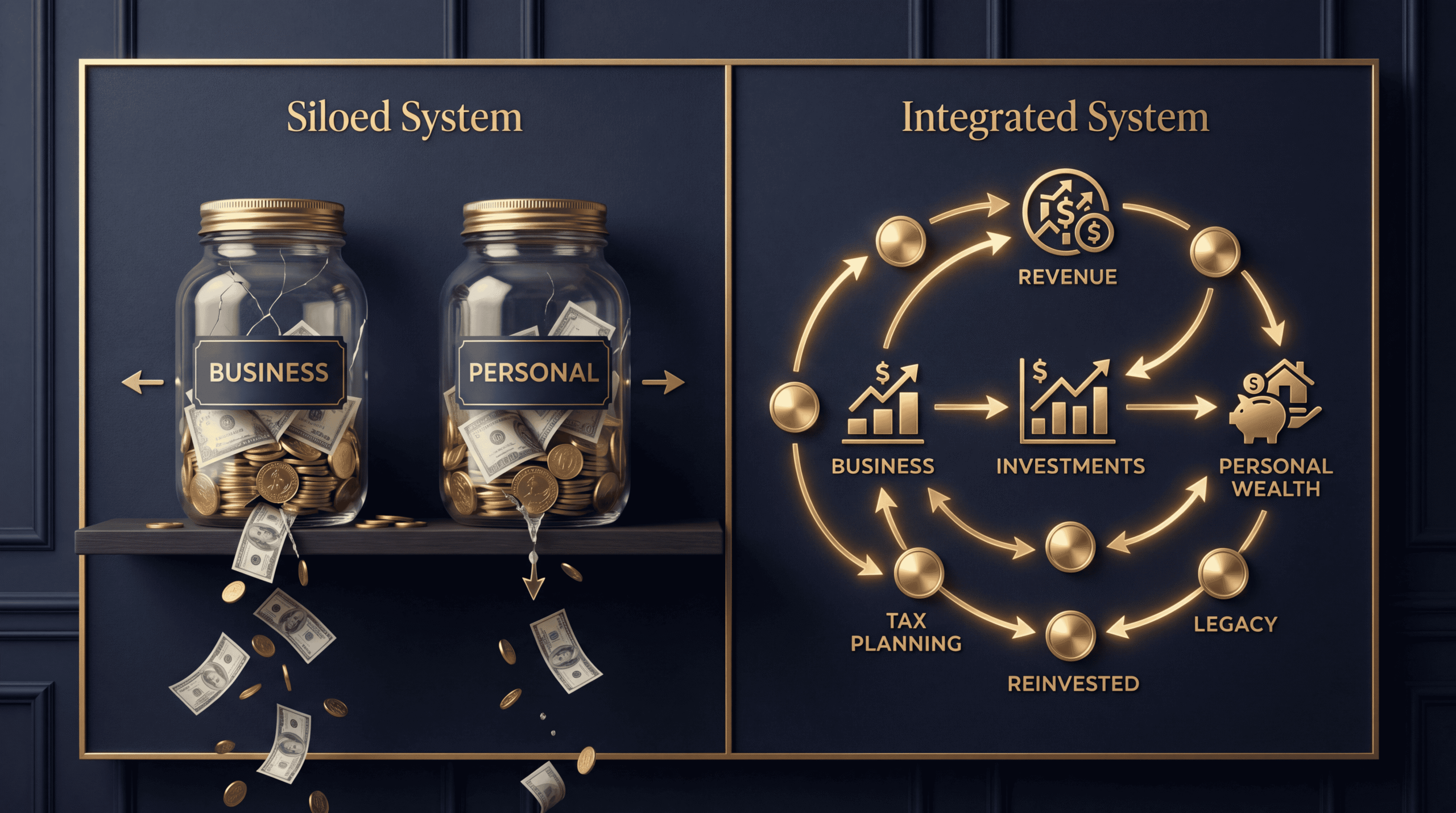

Financial advisors tell business owners to “separate business and personal finances” like it’s gospel. It’s not. This advice keeps entrepreneurs poor while making their accountants feel organized.

The reality? Wealthy business owners don’t manage two separate financial lives. They architect an integrated wealth system where business cash flow, personal expenses, tax strategy, and investment returns work as one coordinated machine.

After advising 200+ business owners with seven-figure net worths, I can tell you the difference between those building real wealth and those trapped on the revenue treadmill comes down to how they think about money flowing through their lives. Let me show you what they’re actually doing.

The Separation Myth That’s Costing You Six Figures

Here’s what happens when you follow conventional advice: You keep business money in the business account, pay yourself a “reasonable salary,” and try to live on that paycheck like an employee. Meanwhile, $200,000 sits in your business checking account earning 0.01% interest while you’re paying 18% on a personal credit card.

According to Federal Reserve data from 2023, small business owners hold an average of $84,000 in low-yield business accounts while carrying $28,000 in personal debt. That’s $1,500 in annual opportunity cost per business owner, compounded by tax inefficiency.

The wealthy don’t operate this way. They understand that business profits, personal living expenses, investment capital, and tax obligations are all parts of one financial ecosystem. Optimizing them separately is like trying to improve your car’s performance by making the engine faster while ignoring the transmission.

What Wealthy Business Owners Actually Do

Let me break down the integrated approach that builds real wealth. These aren’t strategies your accountant discusses because they require thinking beyond next April’s tax return.

Strategy 1: Strategic Personal Expenses Through the Business

Notice I said “strategic,” not “everything.” Wealthy business owners maximize legitimate business deductions that also improve their personal lives. A home office that’s actually used. A vehicle that serves business purposes. Professional development that builds skills. Health insurance premiums run through an S-corp.

The difference? A $50,000 luxury SUV purchased personally costs you $50,000 in after-tax dollars. If you’re in the 35% bracket, you needed to earn $76,923 to buy it. That same vehicle, legitimately used 80% for business, costs your business $50,000 but saves you $14,000 in taxes through depreciation and business use deductions. Your real cost: $36,000.

That’s $40,923 less you need to extract from your business as taxable income. Multiply that across dozens of expenses over a decade.

Strategy 2: Entity Structure Optimization for Tax Arbitrage

Most business owners set up one LLC and call it done. Wealthy entrepreneurs use multiple entity structures to create tax arbitrage between business income, investment income, and personal compensation.

Example: An S-corporation for active business income (avoiding self-employment tax on distributions), a separate LLC for real estate investments (capturing depreciation), and strategic timing of personal compensation to maximize retirement contributions while minimizing tax brackets.

The IRS data shows S-corp owners save an average of $8,000 annually in self-employment taxes compared to sole proprietors at the same income level. Over 20 years at 7% investment returns, that’s $328,000 in wealth accumulation difference.

Strategy 3: Coordinated Cash Flow Timing

Here’s where integration creates alpha. Wealthy business owners time their personal draws, business investments, and tax payments to optimize cash utilization across their entire financial life.

They’re not asking “Should I pay myself this month?” They’re asking “Where does this dollar create the most value right now?” Sometimes that’s reducing personal debt at 6% interest. Sometimes it’s capturing a business growth opportunity with 40% ROI. Sometimes it’s maxing out retirement contributions before year-end for immediate tax arbitrage.

The Psychology Trap: Why Business Owners Self-Sabotage

Research in behavioral finance reveals why smart entrepreneurs fall into the separation trap. It’s called mental accounting—our tendency to treat money differently based on arbitrary categories.

When you rigidly separate business and personal money, you create artificial constraints. You’ll watch business cash pile up “because you might need it” while struggling to fund your kid’s college or watching personal investment opportunities pass by. Meanwhile, inflation erodes that business cash at 3-4% annually.

The psychology works against you in another way: By paying yourself a fixed salary, you disconnect your personal financial success from business performance. This creates a weird employee mentality in your own company. Your business has a great quarter? You get the same paycheck. Your business needs investment? You can’t reduce your draw without triggering personal cash flow panic.

Wealthy business owners think in terms of total wealth optimization, not category protection. They understand that a dollar is a dollar, regardless of which account it’s in. What matters is where that dollar creates the most value after tax implications and opportunity costs.

The Real Separation That Matters

Now, I’m not saying commingle funds like it’s 1985. Legal separation of business and personal accounts is non-negotiable for liability protection and tax compliance. The IRS will disallow your business deductions if you can’t show clear business use, and piercing the corporate veil is real.

But legal separation and strategic integration aren’t contradictory. Think of it like this: Your business and personal finances should have separate houses (accounts) but share a sophisticated communication system (coordinated strategy).

Here’s what proper integration looks like operationally:

- Separate bank accounts with documented transfers

- Every business expense has legitimate business purpose documentation

- Personal draws are regular and documented, not random ATM withdrawals

- Clear bookkeeping that would survive an audit

- But strategic decisions consider total financial optimization, not artificial separation

The Numbers That Matter

Let’s run real numbers on integrated versus separated thinking over 10 years for a business owner earning $300,000 annually.

Separated Approach:

Takes $180,000 salary, leaves $120,000 in business

Pays $45,000 in personal income taxes

Has $135,000 for personal living and investment

Business account grows to $1.2M at 1% interest

Personal investments grow to $400,000 at 7% returns

Total 10-year wealth: $1,600,000

Integrated Approach:

Optimizes compensation mix (salary + distributions + benefits)

Reduces total tax burden to $38,000 through entity optimization

Strategically deploys business cash above 6-month reserves to investments

Captures business expense deductions for legitimate personal-business overlap

Same lifestyle, saves additional $7,000 annually in taxes

Invests business surplus beyond reserves at 8% returns

Total 10-year wealth: $2,100,000

That’s $500,000 more wealth from the same business income. The difference isn’t revenue—it’s integration.

What To Do Instead: Your Integration Blueprint

Here’s your roadmap to stop losing money to artificial separation:

This Quarter:

- Calculate your true opportunity cost. Add up cash sitting in low-yield business accounts. Multiply by (7% market return – current interest rate). That’s what separation is costing you annually.

- Meet with a tax strategist (not just an accountant) who understands entity optimization. Ask specifically about S-corp election, retirement plan options, and legitimate business expense optimization.

- Identify five expenses that legitimately serve both business and personal purposes. Document the business use. Start capturing those deductions properly.

This Year:

- Establish a business cash reserve policy. Calculate 6 months of operating expenses. Everything above that threshold gets strategically deployed—debt payoff, investments, or owner distributions based on highest after-tax return.

- Create a coordinated financial dashboard that shows business cash flow, personal expenses, tax obligations, and investment positions in one view. Make decisions from this integrated perspective.

- Review your entity structure. If you’re still a sole proprietor or single-member LLC making over $80,000, you’re likely overpaying taxes by $5,000-$15,000 annually.

Long-term:

- Build a personal board of advisors who think about integrated wealth: a tax strategist, a financial planner who works with business owners, and an attorney who understands asset protection beyond basic LLC formation.

- Develop a documented compensation strategy that optimizes the mix of salary, distributions, retirement contributions, and benefits based on your total financial picture and tax situation. Review quarterly.

- Create a business succession and wealth transfer plan that treats your business as one asset in your total wealth portfolio, not as your entire financial identity.

The Mindset Shift That Changes Everything

Stop thinking like someone who owns a business and has personal finances. Start thinking like someone who’s building an integrated wealth system where business and personal finances are subsystems of one optimized machine.

The question isn’t “Should I separate business and personal finances?” The question is “How do I legally maintain separate accounts while strategically optimizing across my entire financial life?”

Every dollar flowing through your business, every personal expense, every investment decision, every tax payment—they’re all connected. Optimize them in isolation and you’ll leave hundreds of thousands of dollars on the table. Integrate them strategically and you’ll build wealth that compounds across every dimension of your financial life.

The wealthy don’t separate business and personal finances—they coordinate them with precision.