The Financial Industry Is Selling You the Wrong Benefit

Every financial advisor loves to talk about tax-deferred growth. They’ll bore you to death explaining how your 401(k) contributions lower your taxable income today. But here’s what they’re not emphasizing: employer matching is the single highest-return investment most people will ever access, and the majority of workers are leaving free money on the table.

According to Federal Reserve data from 2023, 23% of workers with access to employer retirement plans don’t contribute enough to capture the full match. That’s not a tax strategy problem—that’s a wealth-building failure that will cost them hundreds of thousands of dollars over their careers.

The obsession with tax breaks is a distraction. Tax deferral is nice, but it’s borrowed time—you’ll pay taxes eventually. A 50% or 100% instant return on your contribution through employer matching? That’s permanent wealth creation that compounds for decades.

The Mathematics of Free Money

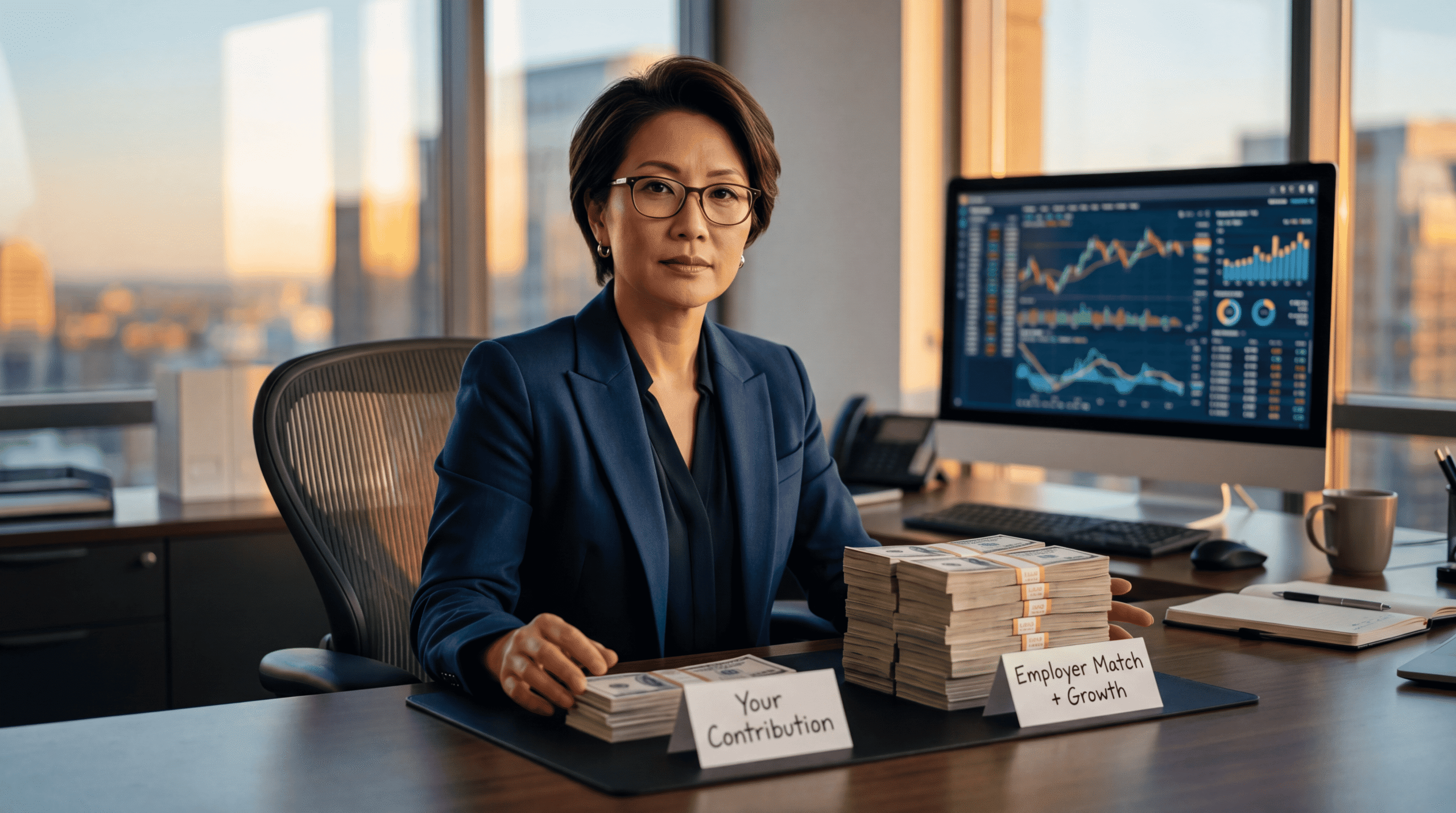

Let’s run the real numbers that financial content rarely shows you. Say your employer offers a 100% match on the first 6% of salary you contribute. If you earn $75,000 annually and contribute 6% ($4,500), your employer adds another $4,500. That’s $9,000 total going into your account.

Here’s where it gets interesting: That employer match represents a guaranteed 100% return before any market gains. Historical market returns average around 10% annually over long periods. Even in a terrible year where the market drops 20%, you’re still up 80% on the matched portion.

Over a 30-year career, assuming 6% salary growth and 8% investment returns (conservative given the match boost), that $4,500 annual contribution with matching grows to approximately $1.1 million. Without the match, the same contribution pattern yields about $550,000. The employer match literally doubles your retirement wealth.

Yet behavioral finance research shows that present bias causes people to systematically undervalue delayed benefits—even when those benefits offer returns that would be illegal if a hedge fund promised them.

The Psychology Trap: Why Smart People Reject Free Money

I’ve watched clients earning six figures fail to capture their full employer match. It’s not ignorance—it’s how our brains process loss versus gain. Contributing to retirement feels like losing money today, even though it’s actually gaining money at rates you’ll never see elsewhere.

The psychological research is clear: We feel losses roughly twice as intensely as equivalent gains. When you increase your 401(k) contribution from 3% to 6%, you experience the smaller paycheck as a loss. The employer match feels abstract and distant, so your brain doesn’t register it as the massive gain it actually represents.

This is compounded by what behavioral economists call “hyperbolic discounting”—our tendency to heavily discount future rewards. A $150 smaller paycheck today feels more significant than $150 in free money that you won’t touch for 30 years, even though that free $150 will compound to over $2,000 by retirement.

The financial services industry hasn’t helped. They’ve trained people to obsess over expense ratios (important, but we’re talking differences of 0.15% annually) while ignoring contribution matching (literally 50-100% instant returns). It’s like worrying about the price of premium gas while someone offers to pay for half your car.

The Real Cost of Partial Participation

Let me show you what leaving money on the table actually costs. Using the same $75,000 salary example with a 6% match, let’s say you only contribute 3%—half of what’s needed for the full match.

You contribute: $2,250 annually. Employer matches: $2,250 (still matching your 3%). Total: $4,500. Over 30 years at 8% returns, you’ll have approximately $510,000.

But if you’d contributed the full 6% to capture the complete match, you’d have $1.1 million. That 3% difference in contribution rate—about $175 per month—cost you $590,000 in retirement wealth. That’s not a rounding error. That’s the difference between a comfortable retirement and working into your seventies.

The Employee Benefit Research Institute found that workers who consistently maximize their employer match accumulate 2.3 times more wealth than those who don’t, controlling for salary and years worked. This isn’t about being smarter or having better market timing—it’s about capturing free money.

Beyond the Match: The Compounding Multiplier Effect

Here’s what makes employer matching even more powerful than the simple math suggests: It front-loads your contributions in a way that maximizes compound growth.

When you contribute $4,500 and receive $4,500 in matching, you’re investing $9,000 from day one of your career. That early money has the longest time to compound. Research on portfolio growth shows that money invested in your twenties and thirties typically represents 70-80% of your retirement wealth, even though it may only be 30-40% of your lifetime contributions.

The employer match effectively doubles your early contributions—precisely when doubling matters most. A $9,000 contribution at age 25 that grows at 8% becomes $90,400 by age 65. That same $9,000 contributed at age 45? Just $19,800 by 65. The match doesn’t just double your money—it doubles your money when time is your greatest ally.

This is why financial advisors who focus primarily on tax optimization are missing the forest for the trees. Yes, the tax deduction is valuable. But the matching contribution is transformational.

What High-Net-Worth Investors Know That You Don’t

When I work with families who have built significant wealth, here’s what I observe: They treat employer matching like the highest-priority investment they’ll ever make. They maximize it before funding taxable investment accounts, before increasing 529 contributions, even before paying down low-interest debt.

Why? Because they understand opportunity cost. If someone offered you a guaranteed 50-100% return in the stock market, you’d mortgage your house to invest. The employer match is exactly that—except it’s real, it’s legal, and it’s sitting in your benefits package being ignored.

Wealthy investors also understand sequence of returns risk. Early contributions matter disproportionately because they have the most time to recover from market downturns. The match doubles your ammunition for riding out volatility. In a market crash, you’re buying at discount prices with twice the firepower.

The middle-class approach of “I’ll increase my contribution when I get a raise” is mathematically wrong. Every year you delay capturing the full match costs you not just that year’s money, but all the compound growth that money would have generated.

What To Do Instead: A Week-by-Week Action Plan

This week: Log into your 401(k) or retirement plan portal. Find two numbers: (1) What percentage you’re currently contributing, and (2) What percentage your employer matches up to. If #1 is less than #2, you’re leaving money on the table.

Next week: Calculate the actual dollar amount. Multiply the gap by your annual salary to see exactly how much free money you’re rejecting. If you’re earning $70,000 and contributing 3% when your employer matches up to 6%, you’re turning down $2,100 annually—plus decades of compounding.

Week three: Increase your contribution rate to capture the full match. Yes, your paycheck will be smaller. The math still overwhelmingly favors this decision. If necessary, cut discretionary spending elsewhere—cable packages, subscription services, dining out. Nothing in your budget offers a 50-100% guaranteed return.

Week four: Set up automatic annual increases. Many plans let you schedule 1% contribution increases each year, often timed to raises. This leverages the psychology of loss aversion in your favor—you never experience the increase as a loss because it comes from money you didn’t have yet.

For those already capturing the full match: Don’t stop there. The IRS allows up to $23,000 in 401(k) contributions for 2024 (plus $7,500 catch-up if you’re over 50). Every dollar above the match still gives you tax-deferred growth and forces automated saving. Research shows that people who maximize retirement contributions build wealth 4-5 times faster than those who only contribute enough for the match.

The Uncomfortable Truth About Retirement

Most retirement advice treats saving as optional optimization—something to do after handling your “real” expenses. That’s backwards. Capturing your full employer match should be as non-negotiable as paying rent.

The data is unambiguous: Vanguard’s retirement research shows that workers who consistently maximize employer matching retire an average of 3-5 years earlier than those with similar incomes who don’t. The difference isn’t that they’re better investors—it’s that they captured free money when it was offered.

The tax benefits of retirement accounts get all the press because they’re easy to explain and the financial industry wants to sound sophisticated. But matching contributions are where ordinary workers can actually build extraordinary wealth.

You’re not competing against hedge fund managers or crypto traders. You’re just capturing a benefit that’s already yours—one that doubles your money, compounds for decades, and requires nothing but raising a single percentage in your benefits portal.

Stop optimizing tax strategies you read about in personal finance blogs. Start capturing the free money your employer is offering right now. It’s the only financial advice that comes with a guaranteed 50-100% return—and most people are still ignoring it.