The Federal Reserve’s favorite inflation gauge just told us something Jerome Powell hoped you wouldn’t notice: inflation isn’t cooling — it’s calcifying into the American cost structure. And unlike the headline CPI numbers politicians love to cherry-pick, the Personal Consumption Expenditures (PCE) index reveals what’s actually happening in your bank account.

After two decades analyzing central bank policy failures from the IMF trading floor to Goldman’s macro desk, I can tell you this: when core PCE stays elevated while the Fed claims victory, you’re watching institutional gaslighting in real-time.

The Number That Matters (And Why Nobody’s Talking About It)

Core PCE — which strips out food and energy to show underlying price pressures — came in at 2.8% year-over-year in recent readings. That’s not a crisis number. That’s something worse: it’s a new baseline.

Here’s what Wall Street won’t tell you: we haven’t seen sustained core PCE above 2.5% outside of a recession shock since 1993. For thirty years, Americans lived in a 2% inflation world. That world is gone.

The Bureau of Economic Analysis data shows something more disturbing. Month-over-month core PCE isn’t declining — it’s oscillating between 0.2% and 0.3%. Annualize that, and you’re looking at 2.4% to 3.6% structural inflation.

What This Actually Costs Real Americans

Let me translate PCE into your life. A household earning $75,000 — roughly the median for a dual-income family — is losing $2,100 annually to inflation above the Fed’s 2% target. That’s not theoretical. That’s the difference between replacing your HVAC system or patching it for another year.

But here’s where it gets vicious: PCE weights spending by consumption patterns. Wealthy households spend more on services that haven’t inflated as much (financial advice, elective medical procedures). Working-class households spend disproportionately on goods and necessities that have inflated faster.

According to Bureau of Labor Statistics expenditure data, households in the bottom 40% of income distribution spend 42% of income on housing, food, and transportation. These categories have seen cumulative inflation of 18-23% since 2020. Do the math: a family making $50,000 has seen effective purchasing power drop by $4,600 over four years.

This isn’t equally distributed pain. This is a structural wealth transfer from wage earners to asset owners.

Why the Fed’s ‘Mission Accomplished’ Narrative Is Dangerous Fiction

The Federal Reserve has been doing a victory lap since inflation dropped from 9% peaks. But they’re measuring against their own disaster. Core PCE above 2.5% means the Fed has failed its mandate — full stop.

Here’s the post-Keynesian reality they won’t admit: inflation is now embedded in price-setting behavior. Corporations discovered they can raise prices 5-8% annually and blame “inflation” while customers have no choice but to pay. Profit margins at S&P 500 companies are near record highs. That’s not cost-push inflation. That’s price-gouging with macroeconomic cover.

The IMF’s latest World Economic Outlook warns that services inflation — the stickiest kind — remains elevated across developed economies. Services inflation in the US is running at 3.9%. You can’t import your way out of services inflation. You can’t drill your way out of it. It requires either wage suppression or demand destruction.

Translation: either workers get poorer through real wage decline, or the Fed crashes the economy. Those are the options.

The Geographic Reality Nobody Discusses

National PCE numbers hide vicious regional disparities. If you live in Phoenix, Miami, or Austin — cities that saw massive pandemic migration — your lived inflation experience is running 1.5 to 2 percentage points higher than national averages.

Housing costs in these metros have increased 35-45% since 2020, according to Zillow rental data. When housing is 30-35% of your expenditure and it’s inflating at 8% annually, your personal PCE is closer to 4-5%, not 2.8%.

Meanwhile, the Midwest and parts of the Northeast are seeing effective PCE closer to 2%. This creates a bizarre two-tier economy where Fed policy that’s appropriate for Cleveland is catastrophic for Charlotte.

What This Means For You

If you’re sitting on cash, you’re losing 2.8% annually in purchasing power — after claiming inflation is “under control.” That’s a guaranteed loss. A $50,000 emergency fund loses $1,400 in real value every year.

If you’re on fixed income — retirees, disability, Social Security — you’re getting destroyed. Social Security COLAs are based on CPI, which is running lower than PCE. You’re getting a 3.2% raise to offset 2.8% PCE, but your actual experienced inflation is probably 4-5%. You’re going backward by $1,000-2,000 annually on a $40,000 benefit.

If you’re a worker expecting wage growth to catch up: it won’t. Real wage growth has been negative or flat for 22 of the last 36 months. The Atlanta Fed’s Wage Growth Tracker shows median wage growth at 4.5%, which sounds good until you realize PCE is 2.8% and your rent went up 7%.

The Credit Card Time Bomb

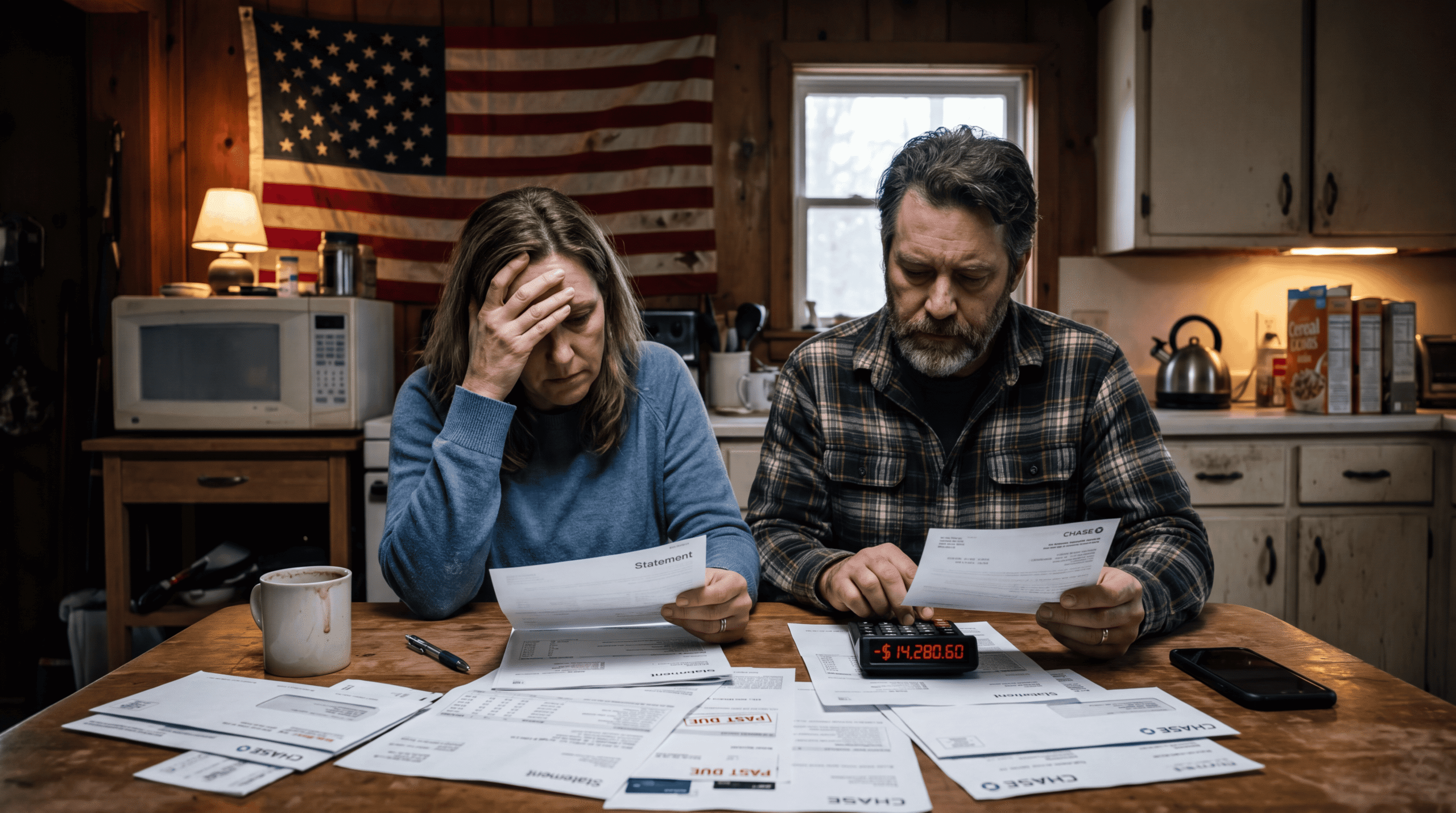

Here’s the second-order effect that should terrify you: American households are financing inflation through debt. Credit card balances just hit $1.13 trillion according to New York Fed data, up 16% year-over-year.

With average credit card APRs at 21.5%, Americans are paying $243 billion annually just in credit card interest. That’s $2,430 per household with credit card debt. You’re not just losing to inflation — you’re paying 21.5% interest to afford inflation.

This is unsustainable. When (not if) we hit the next recession, you’ll see consumer bankruptcy filings spike 40-60%. The 2024-2025 period will look like 2008, except this time households have no home equity to tap and no savings buffer.

Why This Gets Worse Before It Gets Better

The Fed is trapped. They can’t cut rates meaningfully without reigniting inflation. They can’t keep rates high without breaking the labor market. And they can’t admit they’ve lost control of the narrative.

Services inflation — which is 60% of PCE — is driven by wages. Wages are sticky downward. The only way to crush services inflation is to crash employment. That means the Fed needs unemployment at 5-6% to get core PCE to 2%. We’re at 3.7% now.

The Brookings Institution estimates that every percentage point increase in unemployment costs the economy $500 billion in lost output and throws 1.5 million people out of work. The Fed’s 2% inflation target requires sacrificing 2-3 million jobs.

Ask yourself: is Jerome Powell willing to do that in an election year? Not a chance.

What Happens Next: Three Scenarios

Scenario One: Stagflation Lite (60% probability)

Core PCE oscillates between 2.5-3.5% for the next 18-24 months. The Fed holds rates at 5-5.5%, crushing growth but not killing inflation. GDP growth stays under 1.5%. Real wages stagnate. This is the “Japan in the 1990s” outcome — not catastrophic, just a slow grinding erosion of living standards.

Scenario Two: The Breaking Point (30% probability)

Something in the financial system breaks under sustained 5.5% rates. Commercial real estate defaults cascade. Regional banks face liquidity crises. The Fed is forced to cut rates rapidly and inflation reignites to 4-5%. This is the “1970s redux” outcome — high inflation becomes structural, requiring even more painful intervention later.

Scenario Three: The Miracle (10% probability)

Productivity gains from AI and technology adoption genuinely boost supply-side capacity. Immigration reform adds workers. Energy prices collapse on renewable deployment. Core PCE drifts to 2% without requiring demand destruction. This is the optimistic case. I’m not betting on it.

The Bottom Line Wall Street Won’t Say

The inflation crisis isn’t over — it’s normalized. What you’re experiencing isn’t a temporary shock. It’s the new equilibrium. Your dollars will buy less every year for the foreseeable future, and policy makers are out of good options.

The Fed declared victory over inflation the same way Bush declared victory in Iraq in 2003. The hard part isn’t winning the war — it’s winning the peace. And on that measure, they’re failing.

Forty million American households living paycheck to paycheck don’t care about core PCE versus headline CPI. They care that rent is 30% higher, groceries cost 25% more, and their paycheck stretches 15% less far than it did four years ago.

The economists will tell you inflation is transitory. The data tells you it’s permanent. Your bank account tells you which one is right.

Here’s what nobody else will tell you: the Fed’s 2% inflation target was always arbitrary, and defending it will cost you your job, your savings, or both — they just haven’t decided which yet.