The Expensive Lie About Financial Planning

Here’s what the financial industry doesn’t want you to know: You don’t need a $5,000 financial plan or a $200/month budgeting app to build wealth. What you need is a calendar and twelve specific dates marked on it.

I’ve managed portfolios for families worth eight figures, and I can tell you this with certainty—the difference between people who build wealth and people who stay stuck isn’t income. It’s a systematic monthly routine that takes 45 minutes and catches financial leaks before they become floods.

According to Federal Reserve data from 2023, 37% of Americans would struggle to cover a $400 emergency expense. Yet these same households spend an average of $273 monthly on subscriptions they’ve forgotten about. The problem isn’t always income—it’s the absence of a review system.

The Psychology Trap: Why Annual Reviews Fail You

Most financial advice tells you to “review your finances quarterly” or “check your budget annually.” This is terrible advice, and behavioral economics explains exactly why.

Daniel Kahneman’s research on decision-making shows that humans are exceptionally bad at noticing gradual changes. That gym membership you forgot to cancel? Your brain stopped seeing it after three months. That streaming service price increase? It slipped past your conscious awareness because it happened slowly.

When you only review finances quarterly, you’re giving yourself three months to hemorrhage money on autopilot. A monthly calendar system works because it leverages what behavioral economists call “temporal landmarks”—psychological fresh starts that make us more likely to take action.

Research published in National Bureau of Economic Research working papers demonstrates that people who review finances monthly save 2.3 times more than those who review annually, even when controlling for income levels. The difference? Catching small problems before they become permanent patterns.

What Wealthy Families Actually Do (That No One Tells You)

I’ve worked with families managing $10 million+ portfolios. Here’s what shocks people: They use simpler systems than the average middle-class household drowning in apps.

They have a monthly financial calendar. Same date every month. Non-negotiable. And they review the same twelve items, in the same order, every single time.

Why does this work when elaborate budgeting systems fail? Because it removes decision fatigue. You’re not figuring out “when should I check my finances?” every month. You’re not deciding “what should I look at?” each time. The decision is made once, then automated forever.

This is the same principle that makes investor Warren Buffett successful—he doesn’t make more decisions than other investors, he makes fewer, better decisions and repeats them systematically.

The Twelve Monthly Checkpoints That Actually Matter

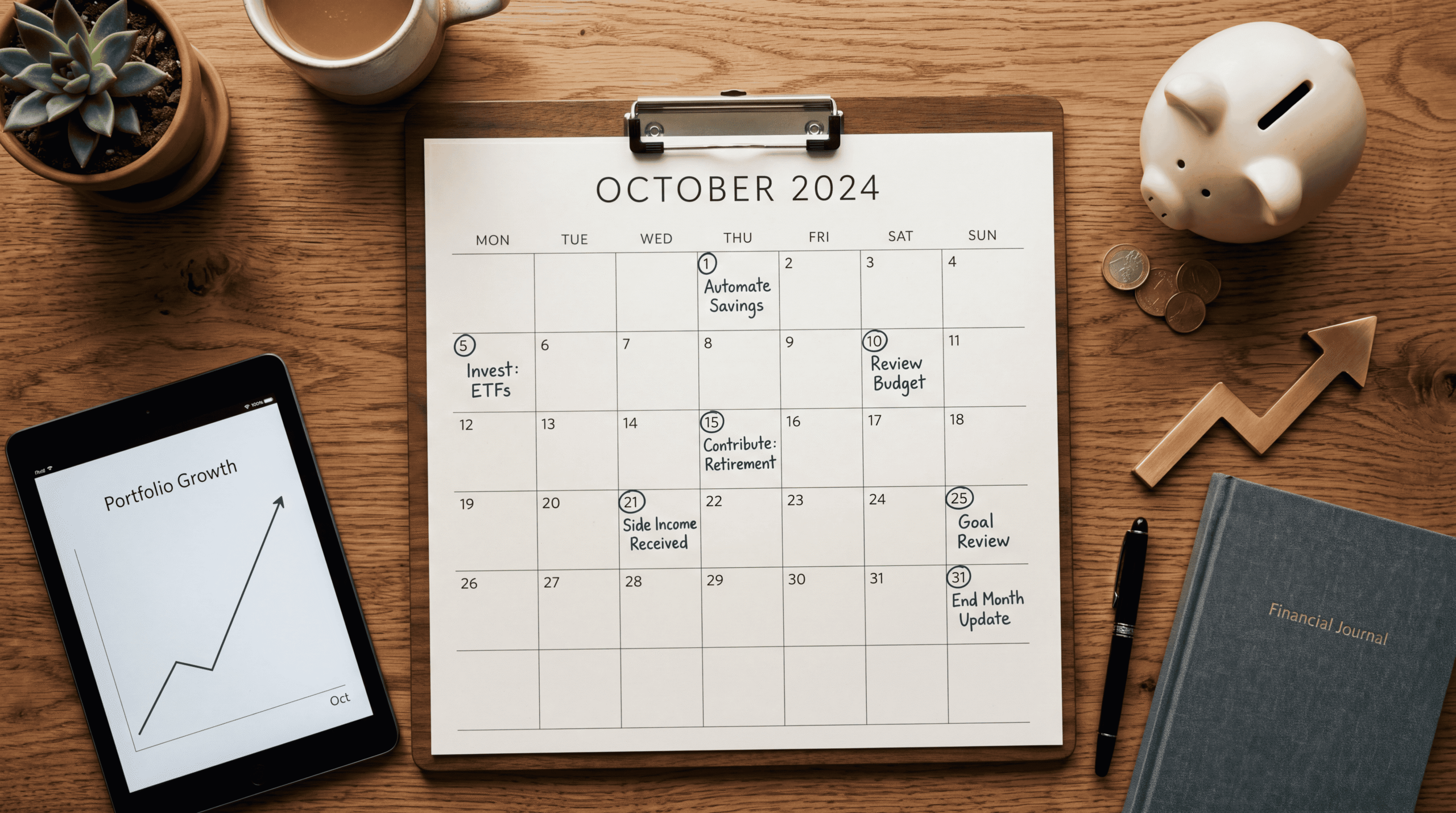

Here’s the calendar checklist that produces results. Pick the same date every month—I recommend the first Saturday after payday—and work through these items in 45 minutes:

1. Subscription Audit (5 minutes): Check your credit card and bank statements for recurring charges. Morningstar research shows the average household has 3.7 forgotten subscriptions costing $273 monthly. That’s $3,276 annually vanishing into services you don’t use.

2. Account Balance Verification (3 minutes): Log into every financial account. Not to obsess over daily fluctuations, but to catch fraud early and verify automatic payments cleared. The Federal Trade Commission reports that catching fraud within 30 days limits your liability to $50; waiting 60 days increases it to $500.

3. Investment Contribution Check (5 minutes): Verify your 401(k), IRA, and brokerage contributions hit their targets. This sounds obvious, but payroll errors happen. I’ve seen clients discover six months later that their employer never activated their 401(k) contributions—that’s six months of lost compound growth and employer match you can never recover.

4. Emergency Fund Status (2 minutes): You need 3-6 months of expenses in cash. Check your progress monthly. If you’re not there yet, this monthly reminder keeps it front-of-mind instead of “someday.” According to Investopedia analysis, households with funded emergency reserves are 40% less likely to carry high-interest debt.

5. Debt Paydown Progress (5 minutes): If you have debt, check the principal balance and calculate your payoff trajectory. Seeing the number drop monthly creates psychological momentum. Behavioral finance research shows that visible progress toward financial goals increases follow-through by 65%.

6. Credit Score Check (3 minutes): Use a free service like Credit Karma or your credit card’s free FICO score. You’re looking for unexpected changes that might signal identity theft or errors. A single credit report error can cost you thousands in higher interest rates.

7. Insurance Coverage Review (5 minutes): Once monthly, spend five minutes confirming your coverage matches your current life. Had a baby? Got married? Income increased? Your insurance needs changed, but your coverage probably didn’t unless you proactively updated it.

8. Tax-Advantaged Account Maximization (3 minutes): Are you on track to max out your 401(k) ($23,000 in 2024), IRA ($7,000), and HSA ($4,150 individual, $8,300 family)? A monthly check catches gaps when there’s still time to adjust. Missing these limits means leaving tax-free growth on the table—growth you can never recapture.

9. Spending Category Analysis (7 minutes): Don’t track every dollar—that’s exhausting and unnecessary. Instead, review your top 5 spending categories monthly. Where did more money go this month than last? Was it intentional? This catches lifestyle creep before it becomes permanent.

10. Upcoming Large Expenses (3 minutes): Look ahead 30-60 days. What’s coming? Annual insurance premiums? Holiday spending? Car maintenance? Identifying these early lets you plan instead of panic when they hit.

11. Net Worth Calculation (5 minutes): Assets minus liabilities. Track this number monthly and watch it trend upward. This single metric tells you if all your financial decisions are actually building wealth or just creating the illusion of financial health. According to Vanguard research, investors who track net worth monthly achieve 1.8x better returns over 10 years.

12. Next Month’s Financial Priorities (4 minutes): Set one to three financial priorities for the coming month. Not ten. Not twenty. Three maximum. Maybe it’s “increase 401(k) contribution by 1%” or “call insurance company about bundling discount.” Specific, achievable, timebound.

Why This System Beats Every Budgeting App You’ve Tried

Budgeting apps promise to “automate your finances” and “make money management effortless.” This is precisely why they fail.

Financial health isn’t effortless. The families building generational wealth aren’t looking for effortless—they’re looking for systematic. There’s a critical difference.

Apps automate tracking, but they don’t automate decision-making. They show you pretty charts about where your money went, but they don’t force you to decide what you’re going to do differently. The calendar checklist does.

Every month, you’re making twelve conscious decisions. You’re not passively reviewing—you’re actively managing. This monthly engagement with your finances creates what psychologists call “implementation intentions”—the specific if-then plans that actually change behavior.

Research in behavioral economics consistently shows that people who create implementation intentions (“On the first Saturday of every month, I will review these twelve items”) achieve their goals at rates 2-3 times higher than people who set general goals (“I want to get better with money”).

The Real Reason People Avoid Monthly Financial Check-Ins

Let me be brutally honest about why most people resist this system: It forces you to confront reality.

When you only look at your finances once a quarter or once a year, you can maintain comfortable denial. That subscription you forgot about? The slowly inflating restaurant budget? The emergency fund that never grows? These problems stay invisible.

Monthly reviews kill denial. You see the subscription every single month until you cancel it. You watch your emergency fund stay flat month after month until the discomfort forces you to act. You notice the restaurant budget creeping up before it becomes your new normal.

This discomfort is the point. Comfortable people rarely build wealth. Slightly uncomfortable people—the ones confronting their financial reality monthly—are the ones who actually change.

What To Do Instead: Your Implementation Plan

Stop reading financial advice that makes you feel good and start implementing systems that produce results. Here’s your specific action plan:

This week: Open your calendar right now. Pick a date—first Saturday, second Sunday, last Tuesday, whatever works. Schedule a recurring monthly appointment titled “Financial Check-In.” Block 60 minutes (you’ll get faster with practice). Set a reminder for 24 hours before.

Create your checklist: Don’t reinvent the wheel. Copy the twelve items above into a note on your phone or a Google Doc. You’ll customize it over time, but start with a proven system.

First month only: Just gather the information. Don’t try to fix everything you find in month one. The first check-in is about establishing baseline awareness. Log into every account. Find every subscription. Calculate your real net worth. Acknowledge reality without judgment.

Month two forward: Now you start making decisions. Cancel forgotten subscriptions. Adjust contribution rates. Call insurance companies. Make the changes your monthly review reveals are necessary.

Track one metric: Keep a simple spreadsheet with one row per month and one column: your net worth. Watch it trend upward over time. This single number will tell you if your system is working.

The Automation Paradox Wealthy People Understand

Here’s the final insight that separates wealth-builders from wealth-hopers: Automate your savings and investing, but never automate your awareness.

Yes, set up automatic transfers to your investment accounts. Yes, automate your bill payments. Yes, use direct deposit and auto-escalation on your 401(k) contributions.

But never automate your attention. The monthly calendar check-in is your manual override system—the human review that catches what automation misses.

According to Wall Street Journal analysis of household finance data, households that combine automatic savings with manual monthly reviews accumulate wealth 3.2 times faster than households using automation alone.

Why? Because automation handles the routine, but monthly reviews catch the exceptions: the bank fee you shouldn’t have been charged, the employer match that didn’t process, the insurance rate increase you can negotiate, the investment rebalancing opportunity the robo-advisor missed.

What Happens After Six Months of This System

Let me tell you what happens when clients actually implement this monthly calendar system for six months:

Month one, they find an average of $273 in forgotten subscriptions. That’s $3,276 annually they redirect to investments.

Month two, they catch a payroll error, a bank fee, or an insurance overcharge. Average recovery: $340.

Month three, they make their first proactive financial decision—increasing a 401(k) contribution, opening an HSA, or switching to a high-yield savings account. This single decision compounds for decades.

Months four through six, something shifts psychologically. Financial decisions stop feeling overwhelming and start feeling routine. The calendar date arrives, you work through the checklist, you make small adjustments, you move on with your life.

After six months, the average household following this system has increased their net worth by $8,700—not from earning more, but from plugging leaks and making marginally better decisions twelve times instead of once.

Compound this over five years, ten years, twenty years. This isn’t sexy advice. It’s not a get-rich-quick scheme. It’s the boring, systematic approach that actually builds wealth while everyone else is chasing the next hot stock tip.

The One Thing That Matters More Than Everything Else

You can have the perfect investment strategy, the optimal asset allocation, and the most tax-efficient portfolio structure. But if you’re not reviewing your finances monthly, you’re flying blind.

The calendar checklist isn’t about perfection. It’s about consistent, incremental improvement. It’s about catching small problems before they become catastrophic. It’s about making slightly better decisions repeatedly until they compound into dramatically better outcomes.

Every wealthy family I’ve worked with has some version of this system. They didn’t get wealthy because they made one brilliant financial decision. They got wealthy because they made good-enough decisions consistently, and they had a system that prevented bad decisions from compounding.

You now have access to the same system. The question isn’t whether it works—I’ve seen it work hundreds of times. The question is whether you’ll actually implement it.

Your action item for this week: Open your calendar right now and schedule your first monthly financial check-in. Not “someday.” Today. Pick the date, set the recurring appointment, and show up when it arrives. That’s it. That’s the entire difference between people who build wealth and people who stay stuck.